I received the following this morning from Tatton Investment Management on the sharp falls in stock markets today and I thought you might find it interesting. For once, it’s not all about Coronavirus!

“While most people spent the weekend dealing with the prospect of the COVID-19 epidemic taking hold of UK life, the financial community woke up this morning to another, different – even if slightly more familiar – type of upset: an oil price shock that unfolded over the weekend.

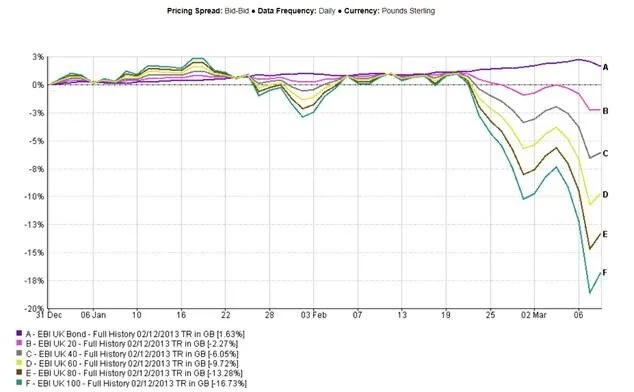

Oil prices have plunged by more than 30% since last week. Together with recent declines, this means that the price of oil has more than halved since the beginning of the year. At the same time, a flight to the perceived safety of government bonds has pushed up bond prices, leading to the lowest yields ever seen on US Treasuries as a result of the inverse relationship between bond prices and their yields.

As a consequence of the double whammy, the already highly nervous stock markets have reacted with what can only be described as panic selling. After falls of around 5% in Asia, European stock markets are opening down by at least as much and in some cases more.

Altogether this news flow will lead many to feel slightly apocalyptic – or at least as anxious as they might have during the darkest days of the financial crisis back in 2008/2009.

But pause for a moment and it becomes clear that this oil price collapse is a total reverse of the most significant oil crisis that took place in the 1970s. This time around, the Saudis decided to push the oil price down, not up, and falling yields take pressures off borrowers, rather than increase it.

This is very different territory compared to previous oil price shocks. So, what is going on?

Following the already significant declines in the oil price since the beginning of the year, there had been widespread expectations that OPEC (plus Russia) would agree to production cuts to stabilise the oil price. It therefore came as a shock to oil traders and their positioning towards rising prices when the opposite outcome occurred over the weekend. Essentially, this means that Saudi Arabia and Russia opted for a resumption of the price war of 2015/2016. Just as now, this strategy was aimed at decimating the competition of US shale oil and gas producers, which require a higher oil price threshold than Saudi and Russia to remain profitable. Just as Trump pursued a strategy of ‘kick ‘em when they are down’ with China last year, it appears the same tactic is now being applied to US oil producers.

Given that the shale producer defaults and the resulting stress in credit markets caused a stock market correction back in Q1 2016, it is not overly surprising that capital markets are following the same script now. Is it likely then that history repeats itself and we are about to witness an even bigger crash than 2016, due to the double whammy of Coronavirus disruptions and oil market upset?

Well, that’s possible in the very short term, but the overall financial, political and economic environment is a different one compared to four years ago. First and foremost, a repeat of the oil price war tactics from back then will no longer carry the same surprise factor. We can expect a much better-informed reaction by the US central bank and government to this renewed onslaught.

Back then, the biggest issue was that mass defaults across the US oil industry would increase the yield costs of corporate credit for all US businesses. Therefore, it is reasonable to expect the Fed will react very quickly to minimise this risk and use its immense quantitative easing (QE) firepower to sell US government and mortgage bond holdings and buy corporate credit to counter any selling pressures. This would also have the effect of easing any ‘flight to safety’ induced supply shortages within government bond markets.

What is more, neither commodity markets nor commodity producers are coming from bubble territory as they did four years ago. This time, there is unlikely to be a similar demand decline from resource industries for manufactured goods, which have already been forced to scale back expansion plans. On the other hand, a halving of the oil price, together with a significant reduction in the cost of borrowing, constitutes a significant stimulus for the global economy and in particular emerging markets, which will additionally benefit from an accompanying fall in the US$.

Our take on this morning’s stock market rout is that faced with this shock surprise action by oil exporters, market participants have become overwhelmed by a doubling up of concerns from the virus disruptions and memories of what happened the last time when oil prices traded at these levels.

We expect some decisive actions from central banks, or at least announcements in this direction. Such actions are unlikely to amount to another round of monetary QE from the Fed, but rather a swapping of government bonds already on its balance sheets with direct purchases of corporate bonds, given that the big falls in government yields from the increased demand in bonds allows them to take supportive action without pushing up yield levels. The Fed has the means to put out this specific fear driven ’fire’, while the economic stimulus effect from the lower cost of energy and of capital should prove to be a very welcome relief over the coming months for the virus disrupted global economy.

At the end of a tumultuous time for stock markets last week, the US stock market rallied hard into the close, leading to a slight weekly gain in those markets overall. This week may well prove similar as there are many more seasoned investors sitting on vast amounts of uninvested cash following years of overextended prices for risk assets.

Perhaps it is worth mentioning that due to unattractively high valuation levels, Warren Buffet’s Berkshire Hathaway fund was at the beginning of the year sitting on uninvested cash of around £130billion. As Warren Buffett is fond of saying: “Price is what you pay; value is what you get. Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.”

As always, if you have any questions concerning this e-mail or any other finance related matter, please do feel to contact me at any time.

With kind regards,

Yours sincerely

{kind=link}

{kind=link}