I am grateful to a friend at 7IM for some of the following:

This news story was everywhere last week (in near identical form).

Let’s not talk about whether Facebook Meta is going to rise or fall in the next few months though….because we have no way of knowing (and neither does anybody else). Instead, let’s talk about how we think about gains and losses. Because in finance we talk in percentages all the time.

“FTSE 100 up x%. Gilts down y%. Portfolio returns are z%.“

But humans don't intuitively work in percentages. We can just about deal with "10% discounts" in a shop, but the minute it gets into "17% rise, followed by a 12% fall", our brains start to struggle.

And, as tends to happen when we’re struggling, we oversimplify.

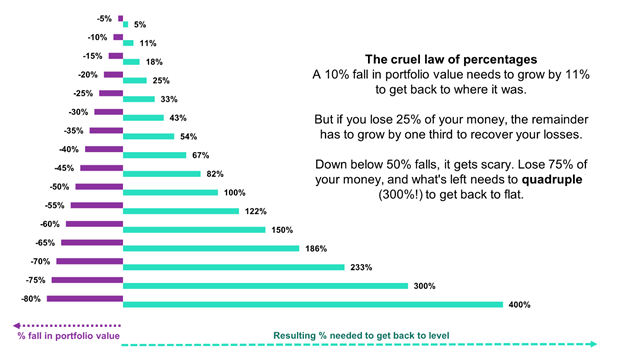

"Up 50% and then down 50% – sounds like it's back where it started ..."

"Down 30%, up 35% – must be higher than before ..."

But that simplification is wrong. And sometimes really wrong.

The chart below shows the reality. And as it's a picture, the brain understands it more easily.

It’s not so complicated when we take a moment to think about it, if £100,000 falls in value by 50% to £50,000, then that £50,000 must double (increase by 100%) to get back to £100,000.

Bringing it back to Meta, and its soaring share price last week.

Since the start of 2022, the stock is still down 45%.

So, glancing at the chart above, it needs another 80% gain to get back to where it was.

Suddenly that 20% day doesn’t seem like nearly enough! Unless of course you happened to buy the stock after it had suffered the worst of the falls.

Volatility of this magnitude is not uncommon with individual stocks that fall into and often spectacularly, out of favour seemingly overnight, but it is less common with a highly diversified portfolio. This is because the economic conditions negatively impacting a particular stock are almost certainly simultaneously positively impacting another; one business’s weakness will often be another’s strength. A diversified portfolio recognises this, leading to a smoother, if not always a positive investment experience. The positive experience comes with fortitude and patience on behalf of the investor.

As always, if you have any concerns about your own financial arrangements or would like to discuss whether you are truly making the most of your money, please do not hesitate to call me.

With kind regards,

Yours sincerely

Graham Ponting CFP Chartered FCSI

Managing Partner